The Drone Stocks Everyone's Buying vs. the Companies That Actually Matter

I mapped every component in a DDP drone. The bottleneck owners and the "DDP stocks" are almost entirely different sets of names.

After the cost model, I went looking for the trade.

If $2,300 doesn’t work — if a compliant DDP drone actually costs $3,500 to $5,000 — somebody captures that spread. After the cost model, I went looking for the trade. The obvious play: buy the drone makers. Kratos, Red Cat, AeroVironment. The names that spike every time a DDP headline drops. Wait for contracts. Collect. It took a weekend of supply chain mapping to understand why that's the wrong bet.

I spent a weekend doing something that felt obsessive: building a full dependency graph of the DDP supply chain. Every critical subsystem, mapped to the component level. Named suppliers. Contract ceilings where I could find them. Tariff exposure. Compliance status. Ten top-level systems. Twenty critical bottleneck nodes. Thirty-five companies scored and tracked.

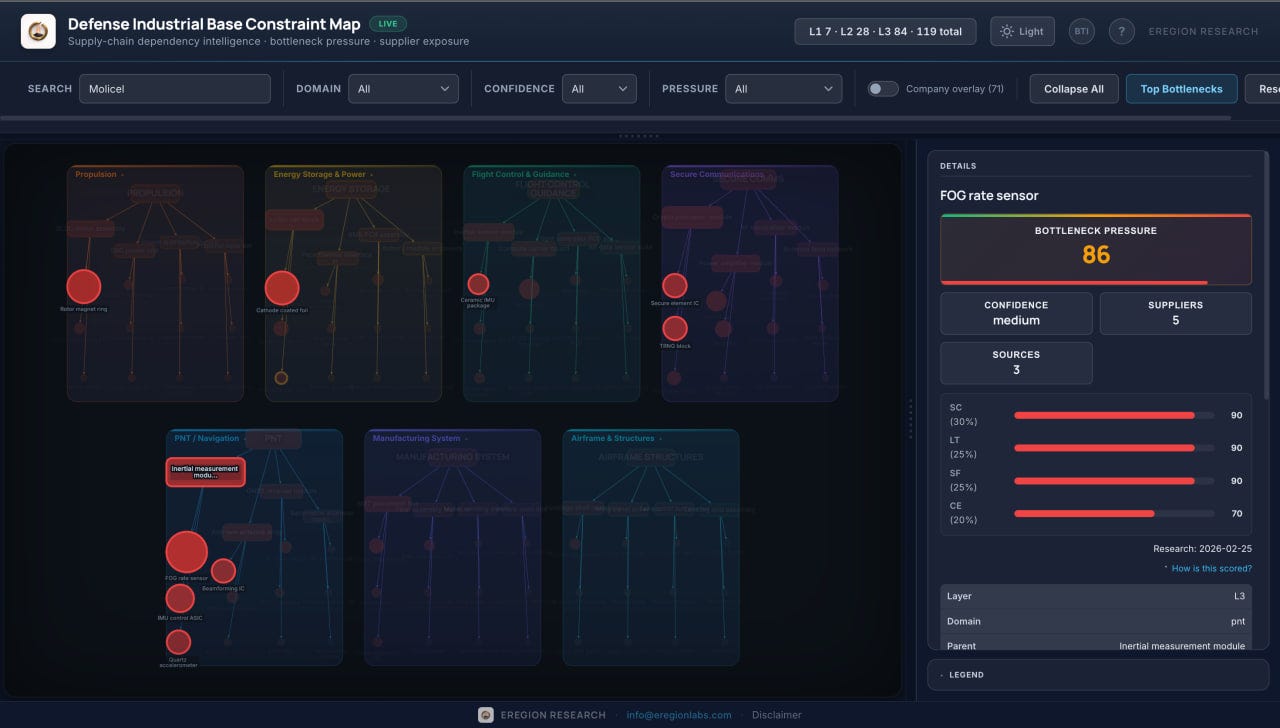

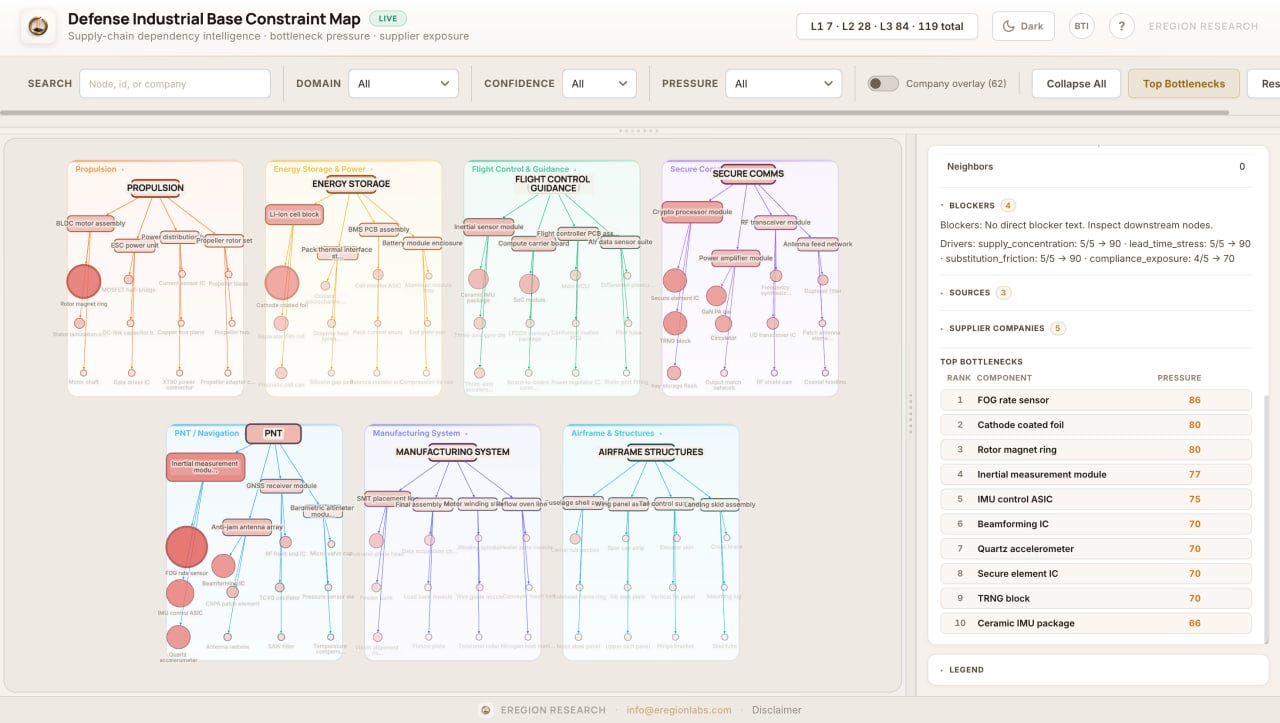

The result is a live interactive constraint map of the entire DDP supply chain. Each node is a component — motors, radios, battery cells, GNSS modules — sized and colored by how tight its bottleneck is. Click a domain to expand it; click a node to see who supplies it, what the blockers are, and how many alternatives exist. You can read this piece without it, but the map is the actual research artifact — everything I found, scored and linked, in one place. Here's what you get:

Browse the full component tree. Seven domains — Propulsion, Energy Storage, Secure Comms, Flight Control, PNT, Airframe, Manufacturing — each expandable into subcomponents down to the individual part level. Eighty-four leaf components total. Click a domain label to expand it; click again to collapse.

See where the program breaks first. Every node is scored on a Bottleneck Tightness Index (0-100) across four dimensions: supply concentration, lead-time stress, substitution friction, and compliance exposure. Bigger, redder nodes are tighter bottlenecks. This is how I identified the components that gate DDP's production timeline — the parts no integrator can design around, ranked by how tight the constraint actually is.

Find the companies behind the components. Toggle the company overlay and diamond-shaped supplier nodes appear, connected to everything they supply. Search any company name or component — the graph highlights matches and expands the relevant domain.

Check the evidence. Click any node and the detail panel shows its BTI breakdown, top suppliers, key blockers, and linked sources. Every claim in the map traces to a source you can inspect.

There's a light mode too — toggle in the top right. Tell me in the comments which one you prefer.

I expected to find the usual defense-supply-chain story: bottlenecks that make costs higher and timelines slower than the Pentagon hopes. Found that. Also found something I wasn’t looking for.

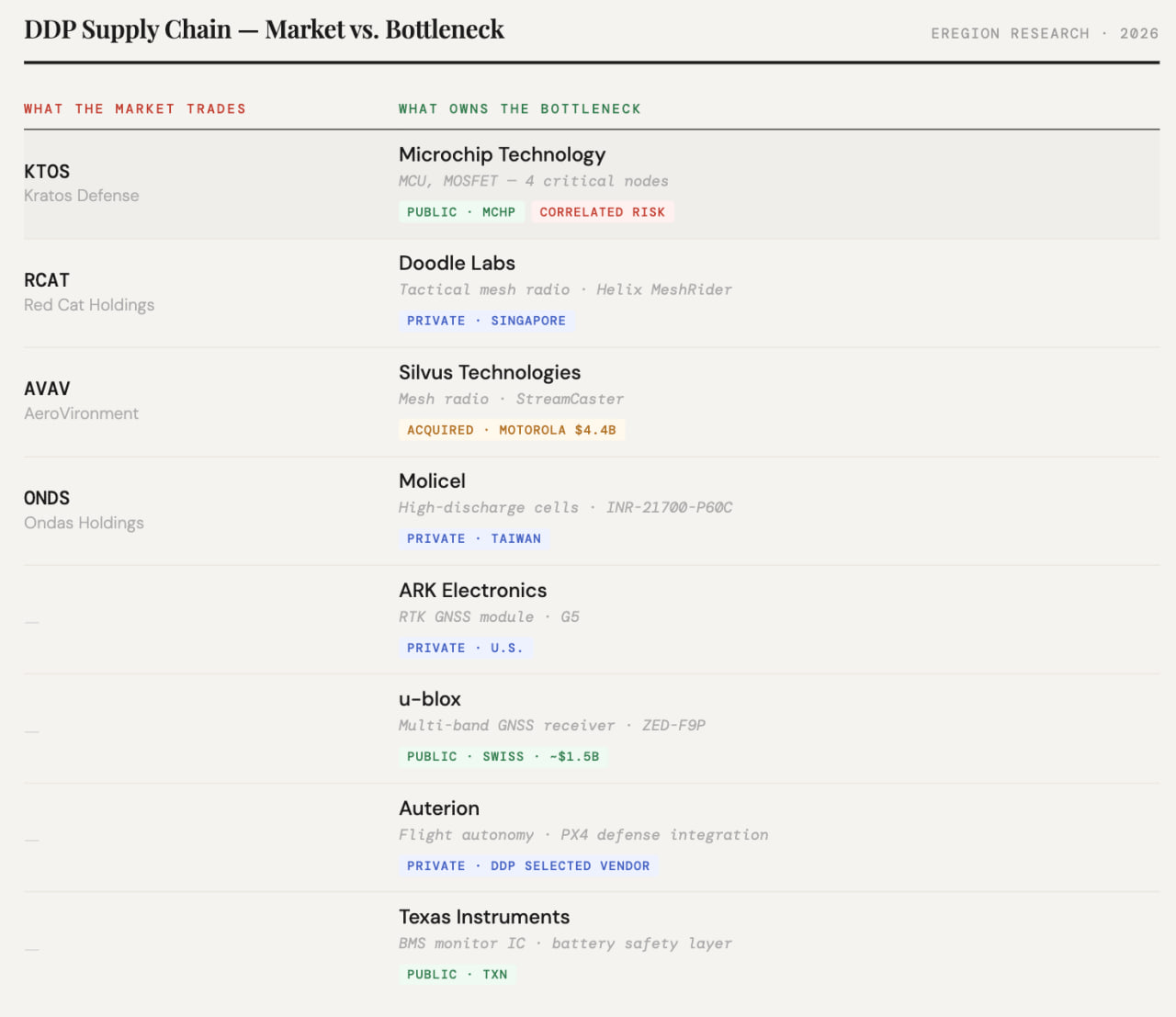

The companies that own the bottlenecks and the companies that trade as “DDP stocks” are almost entirely different lists.

The left column competes for DDP contracts. The right column supplies all of them — the components that go in the drone regardless of which integrator wins the contract. Own a bottleneck component and you have leverage no matter which integrator takes the gauntlet. Be an integrator, and your margin is constrained by what the bottleneck owners charge you.

The market is buying the gauntlet. The market is buying the integrators competing for DDP contracts. The value is in the component suppliers those integrators depend on. Almost no overlap. (The live interactive constraint map allows you to examine every dependency path — click a domain to expand it and see who actually supplies what.)

What follows is what I found working through the bottleneck layer subsystem by subsystem. The pattern that kept repeating: the vendors that matter are private, foreign, or buried inside conglomerates where DDP is a rounding error. And then there’s Microchip Technology — one company across three critical nodes — which is its own kind of problem.

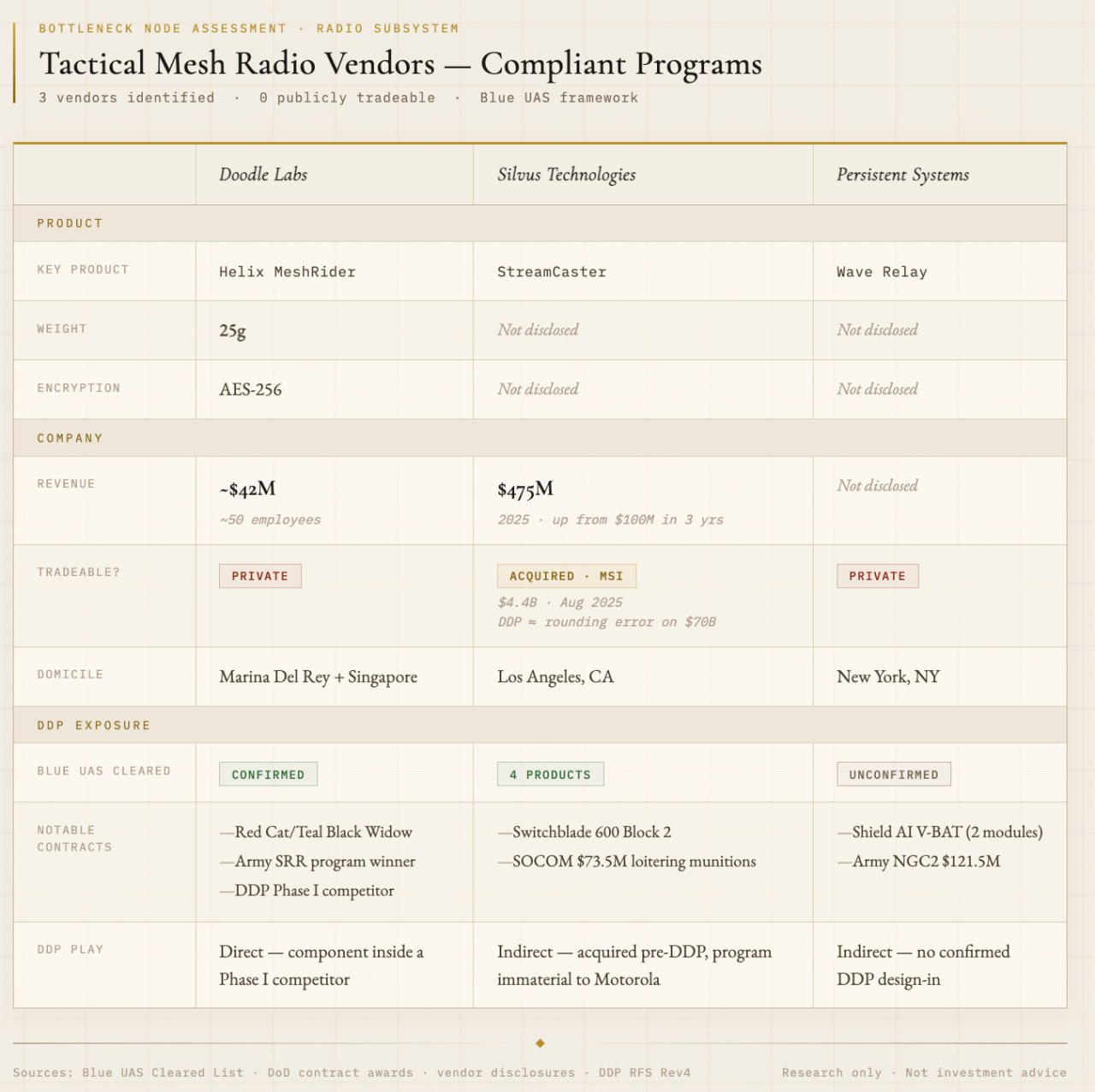

The 25-gram radio

Every DDP drone needs a tactical radio: encrypted, mesh-capable, light enough for a Group 2 platform, NDAA compliant. Three companies show up repeatedly in compliant drone programs.

Doodle Labs makes the Helix MeshRider. Twenty-five grams. Six military frequency bands in one radio. AES-256 encryption. Selected as a component under the Blue UAS Framework. Already flying inside Red Cat/Teal’s Black Widow, which won the Army’s Short Range Reconnaissance program and is competing in DDP Phase I.

Revenue: ~$42 million. Roughly 50 employees. Dual-headquartered in Marina Del Rey and Singapore. Private.

If DDP scales to 300,000 drones and each carries a Helix at $2,000-$5,000 per unit (the range for tactical mesh radios at this tier), that’s $600 million to $1.5 billion in radios — for a company doing $42 million today. That’s a big “if.” But the procurement program is signed.

Silvus Technologies makes the StreamCaster. Revenue hit $475 million in 2025, up from $100 million three years earlier. Seventy-five thousand radios shipped cumulative. The Switchblade 600 Block 2 uses it. SOCOM has it in a $73.5 million loitering munitions contract. Four products on the Blue UAS cleared list.

Motorola Solutions acquired Silvus for $4.4 billion in August 2025 — seven months before DDP launched. That trade is done.

Persistent Systems makes the Wave Relay. Shield AI’s V-BAT ships with two embedded modules. The Army awarded $121.5 million in NGC2 contracts over four months. Private.

Three companies. None of them publicly disclose production volumes. The binding constraints on radios aren’t the ones anyone’s discussing: which encryption level DDP mandates (AES-256 is easy; NSA Type 1 certification takes years), which mesh protocol becomes standard (three proprietary systems that don’t interoperate), and whether 300,000 drones can share RF spectrum without jamming each other.

None of these companies are tradeable as a clean DDP play. The closest proxy is RCAT — it owns Teal, which ships the Doodle Labs Helix — but that’s a bet on one integrator winning the gauntlet. The integrator can lose. The radio goes in every drone regardless.

Three vendors. All private or acquired. (Expand the Secure Comms domain in the live interactive constraint map to see every radio and encryption dependency.)

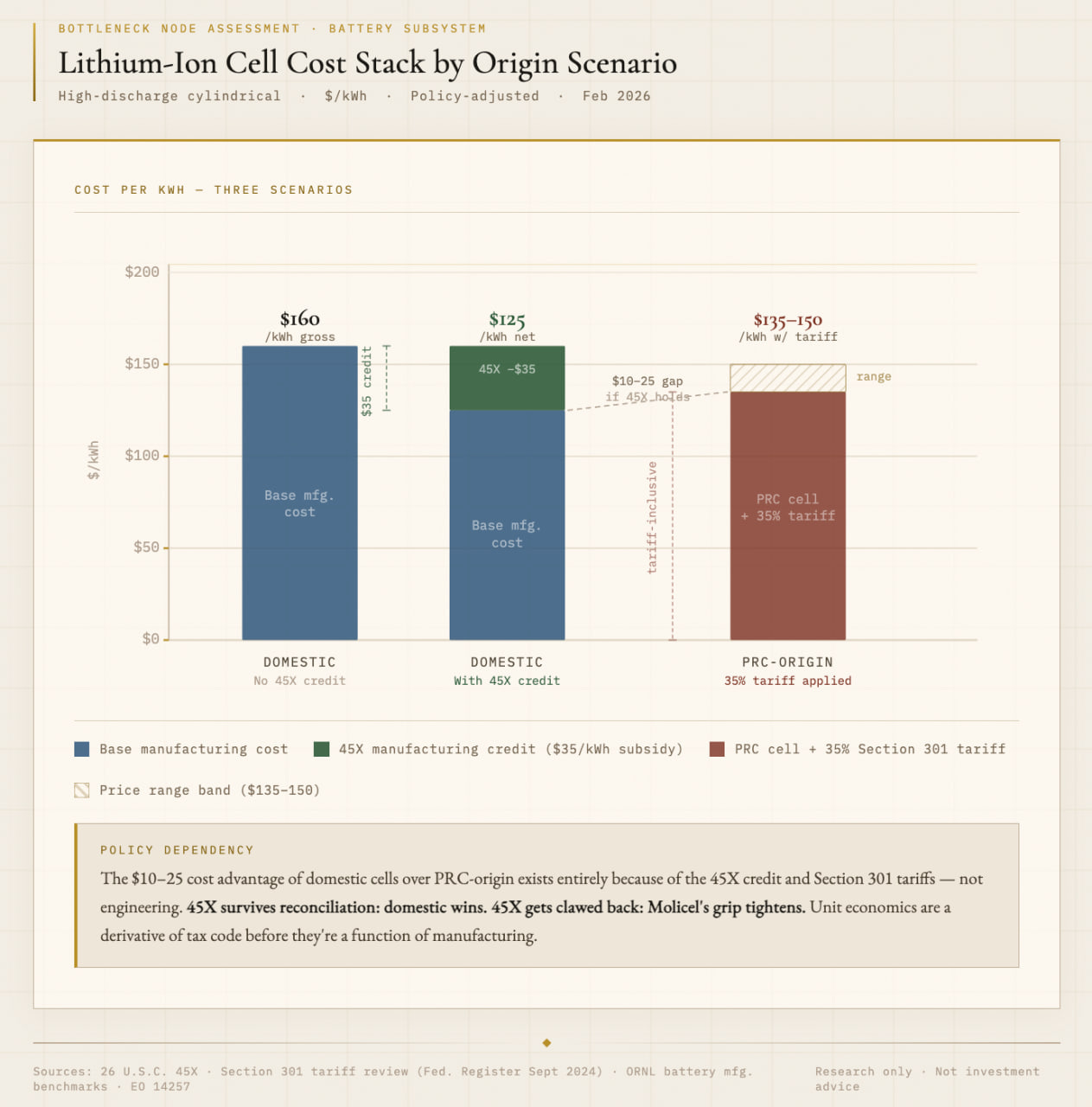

The Taiwanese battery

DDP Phase II draws a bright line: no Chinese cells. Which sounds like supply chain independence until you look at who’s left. The entire program needs a non-Chinese source for high-discharge lithium-ion cells at military scale.

One name keeps surfacing: Molicel. Highest composite score of any company across all forty component-supplier pairs.

Molicel manufactures the INR-21700-P60C — a high-discharge cylindrical cell built for the burst-power profile military drone propulsion demands. Most lithium-ion cells are engineered for consumer electronics or EVs: slow, steady discharge. Drone motors need the opposite. Short, violent draws of current that would cook a consumer cell. The P60C is built for exactly that.

Private. Based in Taiwan.

The obvious question: what about domestic alternatives? Lyten is developing lithium-sulfur cells. Enovix has a silicon-anode factory in Fremont. Amprius is doing silicon nanowire work with Airbus. Real companies, real engineering.

But energy density and discharge rate are different problems. Most next-gen battery companies are chasing energy density — more watt-hours per gram, which matters if you’re building a phone or a long-endurance surveillance platform. Drone propulsion needs something else entirely: cells that can dump violent bursts of current without thermal runaway. The P60C’s value to DDP isn’t that it stores more energy. It’s that it can sustain the current draw of a quad-rotor through a combat mission profile without catching fire.

I haven’t found a domestic manufacturer producing high-discharge cylindrical cells at this performance tier in any meaningful volume. That could change — but not on DDP’s timeline. Lyten’s performance claims still trace back to company-sourced materials, not independent testing. Enovix is tooled for consumer form factors. Panasonic and LG run U.S. lines, but those lines stamp out EV cells — different chemistry, different geometry, different business.

Building a domestic supply chain for military drone cells means convincing a manufacturer to retool for a market that doesn’t exist yet, at volumes that depend on a procurement target my first piece argued is unrealistic, with economics that hinge on a 45X tax credit that may or may not survive. So far, nobody’s building the line.

So DDP has a battery supplier. Taiwan isn't a covered country under the NDAA, so Molicel clears the compliance requirement.

Barely. Taiwan is not China. Democratic ally, security partner, and the NDAA distinction is not arbitrary — it reflects a genuinely different political relationship. But the supply chain crosses the same physical chokepoint. The same strait that TSMC’s semiconductor supply crosses, Molicel’s battery cells cross. A program built to reduce dependence on adversary-disrupted supply chains has its sole battery source 110 miles from the adversary’s coast.

Compliant. Not resilient.

And the economics of that compliance are legislated, not engineered. The 45X battery credit hands domestic cell producers a $35/kWh subsidy — netting $125/kWh against $160/kWh gross cost. PRC-origin cells with the 35% tariff land at $135-150/kWh. Same cell. Same chemistry. Different price — determined entirely by which laws survive the next reconciliation bill. 45X holds and tariffs finalize, domestic producers win. 45X gets clawed back, Molicel’s grip tightens. Across the whole supply chain — semiconductors carry 60% tariff exposure, battery cells 35% — the unit economics of a DDP drone are a derivative of tax code and trade law before they’re a function of engineering.

Three vendors I could find for radios. One dominant supplier for batteries. In Taiwan.

Two companies, one coordinate

A DDP drone needs to know where it is to the centimeter. That means RTK-capable multiband GNSS — GPS plus Galileo or GLONASS, real-time kinematic correction. Without it, the drone can’t navigate, can’t hold a waypoint, can’t prosecute a target.

Two companies kept surfacing in the mapping.

ARK Electronics makes the G5 RTK-GPS. U.S. company, private, small enough that DDP-scale orders would remake the entire business overnight. One of the few components in my graph where I could confirm U.S. assembly. Integrates with PX4-based autopilots, which matters — PX4 is the dominant open-source autopilot in this class and Auterion, the main PX4 defense integrator, is a DDP Phase I vendor.

u-blox makes the ZED-F9P — probably the most widely deployed RTK GNSS receiver in the world. Swiss, publicly traded, small (~$1.3B market cap). Multi-constellation, multi-band, centimeter-level accuracy. The complication: fabless. Wafers come from foundries in Singapore and Taiwan; module assembly runs through Flex in Austria. Clears NDAA scrutiny today. At Phase IV, with full wafer-level provenance audits? The foundry origin becomes the question.

Which could leave ARK Electronics — one small private U.S. company — as the sole compliant navigation module for a program targeting 300,000 drones.

Three radio vendors I could find. One dominant battery supplier. Navigation down to two, possibly one under tighter compliance. At least they’re separate risks — different companies, different failure modes. Right?

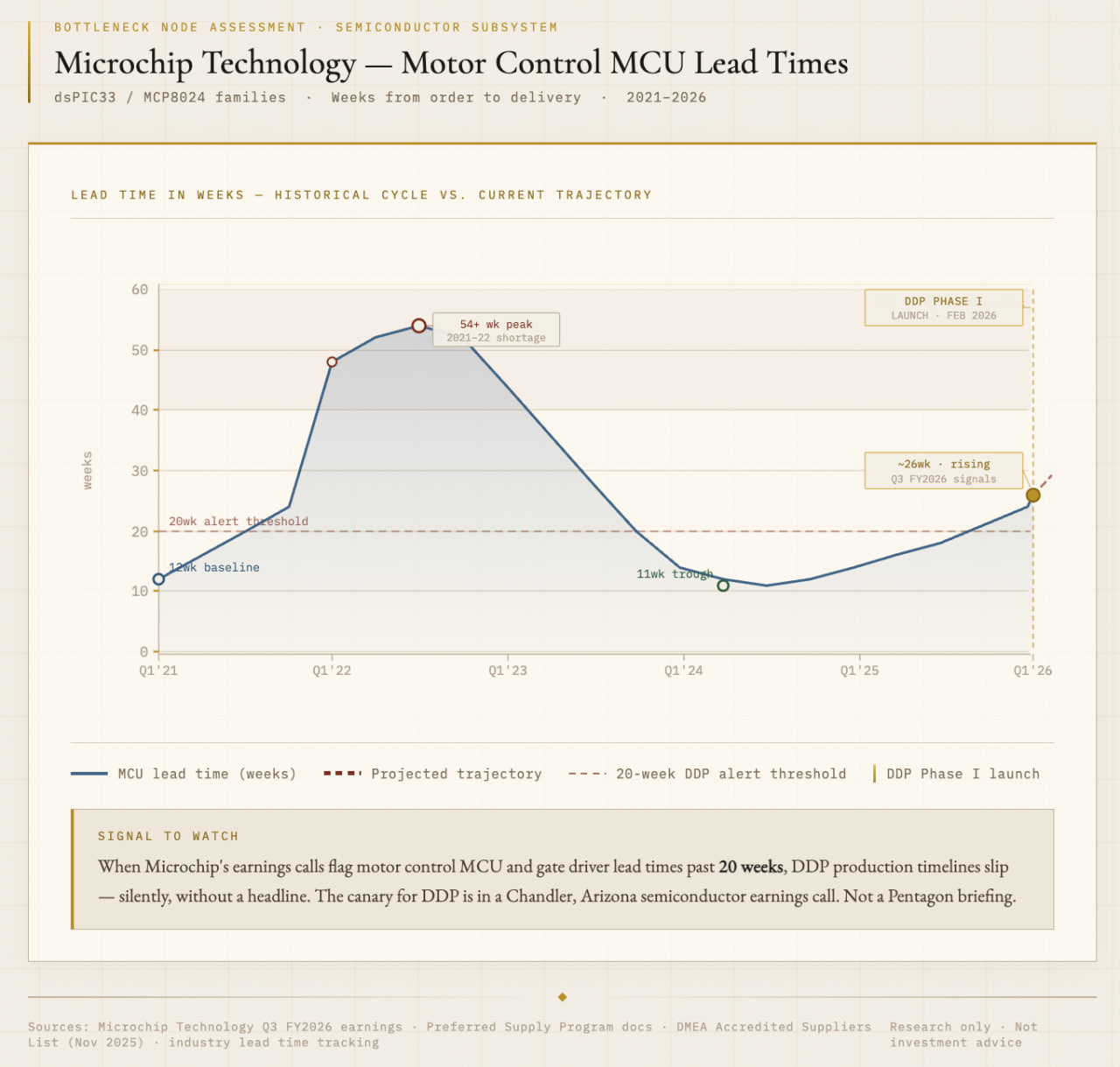

The silent single point of failure

Microchip Technology threads through three of the twenty critical bottleneck nodes. More than any other company. The three: ESC control MCU (dsPIC33 running motor commutation), ESC power stage (MCP8024/8026 gate drivers that switch the motors), and crypto key storage (ATECC608 secure elements up to PolarFire FPGAs for CNSA-grade encryption).

Propulsion and encryption. The motors that keep it flying and the crypto that keeps it yours. One company.

I looked for public evidence of a supply commitment between Microchip and any DDP integrator. Couldn’t find one — no DDP-specific allocation, no priority agreement, no committed backlog in any filing or disclosure I could access. The only relevant public statement is a November 2024 investor relations release saying “most customers receive products in less than 12 weeks” — a portfolio-level marketing claim about their general order book. Maybe agreements exist behind NDAs. But if they do, nobody’s talking about them, and the public evidence points the other way.

During the 2021-2022 semiconductor shortage, Microchip’s most constrained products stretched past 52 weeks — up from an industry-standard baseline around 12. Some were unavailable at any price. Microchip’s response was the Preferred Supply Program: commit to 12 months of non-cancellable orders or lose priority. By late 2021, the most constrained products were 100% allocated through PSP. Not in the program? Not getting chips.

DDP Phase I started February 2026. The integrators are building prototypes. They don’t have 12 months of committed backlog — they probably haven’t settled on which specific Microchip parts they’ll need at scale. So they’re buying spot, at whatever lead time the market gives them, competing for allocation against automotive OEMs with billions in PSP commitments. Toyota gets priority. The drone startup does not.

And the cycle is turning again. Microchip’s Q3 FY2026 earnings: revenue up 16% year-over-year, backlog growing, forward guidance for the March quarter up nearly 30%. Industry tracking shows certain MCU families already at 20-30 weeks. Management language on the earnings call: lead times “bouncing off the bottom,” extending “for certain products.”

The risk isn’t any single part’s lead time. It’s correlated invisible failure. One allocation decision delays propulsion and encryption simultaneously. These aren’t in the same physical subsystem — an integrator troubleshooting a motor delay wouldn’t naturally check their encryption timeline. But both source from Microchip. They fail together. And nobody realizes it until two domains are behind at once, for the same invisible reason.

Microchip does have DMEA trusted supplier accreditation — through Microsemi, their subsidiary that makes FPGAs and radiation-hardened space components. The motor control MCUs and gate drivers that DDP needs? Commercial product lines. Almost certainly not covered.

Nobody appears to be managing this. No multi-source qualification. No buffer stock. No government-directed allocation. The gauntlet structure actively discourages it — integrators competing on price reach for the cheapest available parts and worry about supply security after they’ve won.

I should be clear about what I’m assuming here. I don’t know which specific Microchip parts DDP integrators are designing in. Microchip, along with STMicro and TI, dominates motor control MCUs — the dsPIC33 and MCP8024/8026 are the default for this class of application. But “most likely supplier” and “confirmed supplier” are different statements. What I can say: if the integrators follow the standard design path, the concentration risk is real. And the gauntlet structure gives them every incentive to follow the standard path.

Can you trade it? Microchip is public (MCHP). But DDP is noise to them — A&D is 17-18% of revenue, DDP drone MCUs a fraction of that fraction. You don’t buy MCHP for DDP exposure. You monitor MCHP. When their earnings calls flag motor control MCU and gate driver lead times past 20 weeks, DDP production timelines are in trouble. Nobody in the drone conversation will be talking about it.

The canary for DDP is in a Chandler, Arizona semiconductor earnings call. Not a Pentagon briefing. (Search "Microchip" in the live interactive constraint map to see all three nodes light up across two domains.)

The bottleneck that moves

There’s a version of DDP’s future where the radio problem dissolves entirely. Doesn’t solve the bottleneck. Relocates it.

Ukraine is already there. By early 2026, estimates put fiber-optic FPV drones at somewhere between 5% and 15% of production along the front — a physical wire unspooling behind the drone, zero RF emissions. Unjammable. A growing number fly with no communication link at all: onboard AI making its own guidance decisions in the terminal phase. No radio. No signal to jam. No human in the loop for the last three seconds.

If the answer to “how do 300,000 drones communicate?” turns out to be “many of them don’t,” the radio bottleneck weakens. But it doesn’t disappear. It shifts to whoever can certify autonomous navigation for military use.

Two companies. Shield AI — Hivemind autonomy stack, drones operating GPS-denied and comms-denied. Private, $5.3 billion valuation as of March 2025. Auterion — defense-certified integration layer around PX4, the dominant open-source autopilot in this class. Their moat isn’t technical. PX4 is open source; anyone can read it. The moat is regulatory: audit trails, compliance docs, the institutional trust of being the company the Pentagon already works with. Selected DDP vendor per RFS Rev4. Private.

The architecture may evolve. The pattern doesn't: whoever owns the critical node is private, acquired, or buried inside a conglomerate where DDP is a rounding error.

The trade that might not exist

There may not be a clean public equity trade here.

The bottleneck owners — Doodle Labs, Molicel, ARK Electronics, Persistent Systems, Auterion, Shield AI — are private. Silvus is inside Motorola, a rounding error on $70 billion. TI and Microchip are conglomerates where DDP is immaterial. The publicly traded drone companies are integrators whose margins are constrained by component suppliers and trade policy they don’t control.

Demand is everything the market says: real, structural, bipartisan, roughly a billion dollars and growing. Supply is everything it isn’t saying: fragmented, policy-dependent, concentrated in companies you can’t buy. That gap — between who the market is betting on and who actually controls supply — is the mispricing this piece is about.

Most defense-tech analysis stops at “the theme is real, buy the names.” The theme is real. The names are wrong. And the right names aren’t available.

But this isn’t just an argument about what not to buy. The signals that matter won’t show up in drone stock coverage or Pentagon press briefings. They’ll surface in semiconductor earnings calls, tax policy markups, and contract award databases that nobody in the defense-tech conversation is reading. I’m reading them.

Microchip lead times. Motor control MCU and gate driver lead times past 20 weeks mean DDP production timelines slip. Silently, without a headline. I’ll flag it when the language changes.

The 45X credit. Battery credit survives, domestic cell production eventually pencils and the DDP cost model works at the high end. Credit dies, the program needs a tariff waiver or the unit economics break further. Every reconciliation bill is a data point.

DDP Phase I Gauntlet results. Preliminary results expected around March 10. Which integrators advance tells us which supply chains the Pentagon is betting on. Watch how aggressively the funnel narrows — fewer survivors means more pricing power for the bottleneck suppliers feeding all of them.

The autonomy shift. If DDP Phase II or III moves toward comms-denied autonomous operation, the radio bottleneck dissolves and the autonomy bottleneck takes over. Shield AI and Auterion become the names. Both private. The untradeable pattern persists.

The drones will get built. The money will flow. And the companies with the most leverage over that flow — the ones sitting at bottleneck nodes — are mostly in places you can’t buy a share of. That’s not the finding I wanted. It’s what the dependency graph kept showing me.

The 300,000-drone program’s timeline may hinge on the commercial MCU order book of a semiconductor company in Chandler, Arizona where DDP wouldn’t move the needle enough to warrant a mention on an earnings call.

This is the second piece in our DDP supply chain series. The first piece showed why $2,300 drones don’t exist yet. This one maps who makes the components and where the value actually accrues. The third piece will cover the power grid bottleneck underneath all of this — the constraint that nobody can build their way out of. If you’re interested in the interactive supply chain graph, explore it here.

Disclosure

No positions in KTOS, RCAT, AVAV, ONDS, MCHP, MSI, or TXN. This is research, not investment advice. The supply chain mapping is built from public sources — DoD contracts, SEC filings, vendor product pages, Blue UAS cleared lists, and industry databases. Do your own work.

Sources

DDP RFS Rev4 via NSTXL (Phase I-IV structure, pricing, domestic sourcing requirements)

SAM.gov notices N0016426SNB20, N0016426SNB26 (authoritative program captures)

DoD contract award: Collins ARC-210, 8,493 radios, Sept 2024

DoD contract award: GPS Source, up to 4,000 antennas, June 2024

DoD contract award: BAE Systems MGUE, Jan 2025

Microchip Technology Q3 FY2026 earnings, IR disclosures (Dec 2025)

Microchip Preferred Supply Program documentation

DMEA Accredited Suppliers List (Nov 2025)

Motorola Solutions acquisition of Silvus Technologies, $4.4B (Aug 2025)

Silvus Technologies revenue and contract disclosures

Doodle Labs product pages, DigiKey pricing, SRR program announcements

Persistent Systems NGC2 contract awards ($87.5M Feb 2026, $34M Oct 2025)

DIU Blue UAS Framework and Cleared Components List

AeroVironment Switchblade 600 Block 2 radio integration disclosures

Shield AI V-BAT Wave Relay integration, Hivemind autonomy stack

Molicel INR-21700-P60C datasheet; ORNL battery cell manufacturing benchmarks

ARK Electronics G5 RTK-GPS product documentation

u-blox ZED-F9P product datasheet, GPS.gov specifications

Auterion Government Solutions: DDP RFS Rev4 vendor selection, PX4 VIO integration

USGS Mineral Commodity Summaries 2026 (rare earth, copper, lithium)

26 U.S.C. 45X (battery manufacturing credit)

Section 301 tariff review, Federal Register Sept 2024

EO 14257 (PRC additional duty)

ORNL/DOE battery manufacturing cost benchmarks

Ukraine drone warfare reporting: fiber-optic FPV, AI-guided autonomous systems (United24, MIT Technology Review, New Geopolitics)